Easy access to information and digitization of the mutual fund industry have made investing a quick and easy process, allowing investors to express their investment decisions to buy and sell at the click of a button. But, is the average investor really better off with the ability to quickly act on these opinions?

Over the course of our lives we are conditioned to believe that success only comes to those who actively work towards it. We tell our kids that they will succeed at school only if they work hard and study diligently. Though this may be true for most things in life, it isn’t necessarily true for investing. Even though it may sound counter-intuitive, the average investor may be better off by following a “do-nothing” approach to investing.

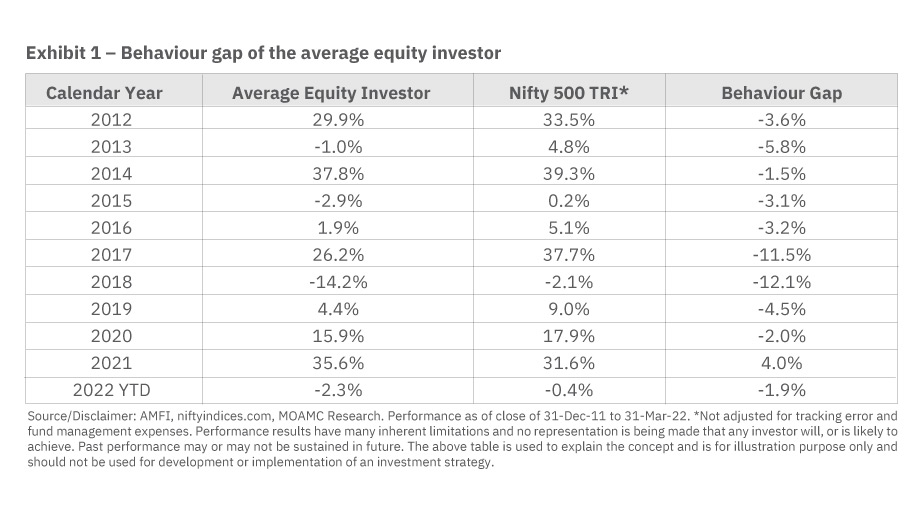

The average equity investor underperforms

To understand how well the average equity investor performs (investor return) in comparison to the market (investment return), we analyzed the net fund flows into open-ended Equity schemes over the last 10 years. A simple IRR calculation of these net flows can help approximate returns experienced by the average equity investor. The difference between the returns generated by the average equity investor and the Nifty 500 TRI (proxy for equity market) is highlighted in the “Behavior Gap” column. A negative “Behavior Gap” implies that the average investor underperformed in that period while a positive reading implies outperformance.

Results show that the average investor has underperformed the market in 9 out of the last 10 calendar years (excluding 2022 YTD) with significant underperformance in 2017-18 and a surprise outperformance in 2021. Over the entire period, the average equity investor was worse off by 4.7% per annum primarily due to discretionary investment decisions of buying and selling.

The average debt investor fares better

The same analysis conducted for the average debt investor yielded similar results with underperformance noted in 7 of the last 10 calendar years. Over the entire period, the behavior gap for the average debt investor was considerably smaller at just 0.4% per annum. The smaller underperformance may be partially attributed to a much larger share of institutional participation in the debt-oriented mutual fund categories who are likely to be less erratic in their investment decisions as compared to retail investors.

What causes the behavior gap?

The behavior gap is typically caused by irrational investment decisions taken by investors that are often based on emotions. An example of this is making investment decisions based on recent performance. You would be familiar with the common “Past performance is no guarantee of future results” disclaimer If you have looked at any marketing material published by mutual fund houses in the last couple of decades. Yet, a very large chunk of investors continues to base their investment decisions of buying and selling on recent performance.

Source/Disclaimer: AMFI, niftyindices.com, MOAMC Research. Performance as of close of 31-Dec-11 to 31-Mar-22. Performance results have many inherent limitations and no representation is being made that any investor will, or is likely to achieve. Past performance may or may not be sustained in future. The above table is used to explain the concept and is for illustration purpose only and should not be used for development or implementation of an investment strategy.

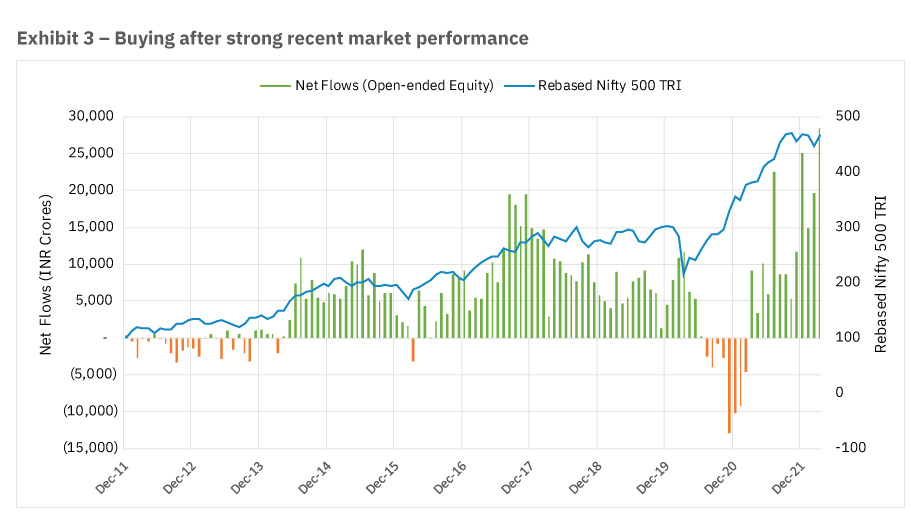

If we look at the net fund flows into open-ended Equity schemes over the last 10 years, we can clearly see that there has been a very large amount of inflows just after the market has run up. This outcome bias, making decisions based on the outcome of recent events, ends up with the average investor “buying high and selling low”.

Another example of irrational investor behavior is believing that you can effectively and consistently time the market. When the market crashed in early 2020 due to the Covid-19 pandemic, there was a visible spike in the net inflows into equity schemes. The average investor had made hay of the opportunity and bought when the market was low. However, this was followed by 8 consecutive months of net outflows (of INR ~47k crores) from Jul-2020 to Feb-2021 as the markets continued to climb higher and higher. The average investor got cold feet and sold very early, having failed to foresee this tremendous bull run in the Indian equity markets.

What should investors do?

To help improve outcomes of their investment decisions and bridge the behavior gap, investors should keep the following things in mind –

- Don’t try to time the market – instead investors should keep investing consistently at a predefined frequency and not let the twists and turns of the market dictate their investment decisions. It’s important to remember that “time in the market” is more important that “timing the market”. Starting a monthly SIP can be a great way to inculcate this positive behavior and build wealth over the long-term investing.

- Buy the market – investors can look at investing in a low-cost passive fund that tracks a broad-based index. The Nifty 500 Index covers ~91% of the listed universe of companies in India. Therefore, investors can gain exposure to the entire domestic equity market by buying a single fund.

- Diversify your portfolio – investors should make sure that their investment portfolio is well diversified across different asset classes (Gold, International Equity, Debt). Having assets that have low correlation to each other helps smoothen the investment journey. In fact, Nobel Prize winner Harry Markowitz famously regarded diversification as the “only free lunch in investing”.

This article was covered by mintgenie on 20th April 2022

Author: Raghav Avasthi, Research Analyst, Passive Funds, Motilal Oswal AMC

Co-author: Mahavir Kaswa, Head of Research, Passive Funds, Motilal Oswal AMC

Disclaimer: This article has been issued on the basis of internal data, publicly available information and other sources believed to be reliable. The information contained in this document is for general purposes only and not a complete disclosure of every material fact. The indices mentioned herein is for explaining the concept and shall not be construed as an investment advice to any party. The information / data herein alone is not sufficient and should not be used for the development or implementation of any investment strategy. It should not be construed as an investment advice to any party. All opinions, figures, estimates and data included in this article are as on date. The article does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. The statements contained herein may include statements of future expectations and other forward-looking statements that are based on our current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Readers shall be fully responsible/liable for any decision taken on the basis of this article. Mutual Fund investments are subject to market risks, read all scheme related documents carefully.